ANALYSIS

by Timothy Pang and Daniel Chancellor

Around one-quarter of active drug development now has a Chinese origin, with particular emphasis in biologics, cell therapies and cancer R&D. While the appetite for these assets among multinational pharmaceutical companies remains strong, the financing crunch that is throttling investment into start-ups is being felt particularly keenly in China. In such a landscape, domestic biotech companies will need to prioritize reliable near-term revenue streams while keeping global ambitions in mind. A domestic Amgen- or Regeneron-like success story may yet be inevitable, although steady progress is far more likely than a sudden growth spurt.

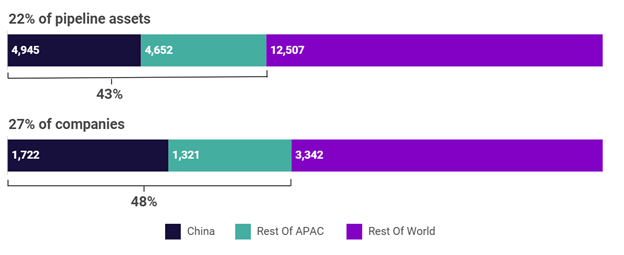

Having broken through the 20,000 mark in 2022, the global biopharma pipeline has continued to grow and now totals more than 22,000 assets under active development. In recent years, while the pace of expansion has moderated in Western markets, China has dramatically increased its R&D footprint.

As shown in Exhibit 1, there are now around 5,000 drugs under active development by China-headquartered companies, part of an ecosystem of around 1,700 drug developers. Remarkably, it was only five years ago that Chinese companies collectively possessed just 1,000 drug programs, and 10 years ago the figure was a mere 200. This growth spurt over the last decade has resulted in Chinese companies now laying claim to around one-quarter of all global R&D.

Exhibit 1: Chinese Share of Global R&D, Assets, and Companies

Source: Citeline, Pharmaprojects

Among the totals, China possesses clear strengths in biologics, cell therapies and cancer drug development. In each of these three hot growth areas for research, China has a larger-than-expected footprint. This does not come at the expense of overall diversity, with the presence of emerging domestic gene and RNA therapy platforms and large numbers of clinical trials across the spectrum of therapeutic areas and diseases.

Alliances in Vogue

This engine for new drug creation has allowed the capture of domestic market share, but also attracted the attention of multinational pharmaceutical companies. Particularly for validated drug classes, Chinese biotechs have been quick to create their own versions using platform technologies. The classic example is in the programmed cell death protein 1/ligand 1 (PD-1/L1) market, where the total now stands at 12 approved China-originated monoclonal antibodies. This pattern is also being played out across a multitude of drug targets, even for those still in the developmental stage. Over half the anti-TIGIT pipeline is Chinese, while home-grown biotechs are often leading the developmental effort for new chimeric antigen receptor (CAR) T-cell designs.

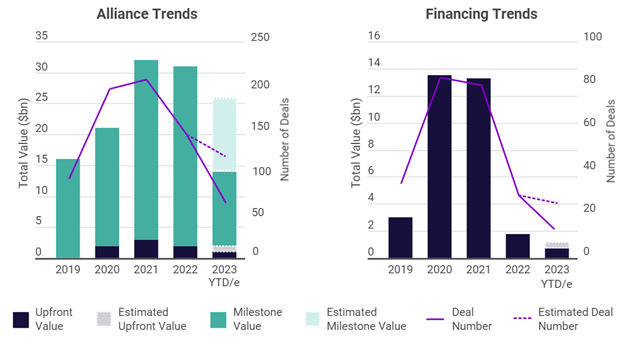

These assets are highly attractive for multinational pharmaceutical companies looking to license their way into emerging drug classes. Exhibit 2 shows the number (line) and value (bars) of such alliances, split by upfront payments and potential milestones. Each year, Chinese biotechs are securing around $2 billion to $3 billion in upfront fees and milestones of up to $30 billion, in addition to any separate financing or product revenue streams. While there has been a slight drop from the peaks of 2021, perhaps relating to the regulatory realities of commercializing assets without US-based trials, demand is still robust.

These alliances are even more important to Chinese biotech firms considering the throttling of external investment over the last 18 months. While the biotech downturn has been apparent globally, its effects have been felt keenly in China. Financing peaked in 2020 and 2021 with around $13 billion raised in total, although this plummeted to just $2 billion in 2022, and 2023 may finish even lower. For the many clinical-stage, pre-revenue biotechs, the stark drop in the capital markets leaves growth ambitions on hold.

Exhibit 2: Chinese Biopharma Dealmaking Trends Since 2019

Source: Citeline, Biomedtracker

Countermeasures to Navigate Near-term Challenges

This short-term pressure leaves many forced to consider strategic countermeasures in order to preserve cash runways and chart a path to market for lead assets. Most immediately, those without revenue streams must recalibrate business operations and R&D expenses to bridge the downturn. On the costs side, this can include scaling back of pipelines and headcount, while capital expenditure can be deferred. Short-term funding solutions are also essential, such as scaling alliance structures in a way that eschews milestone payouts in favor of immediate cashflow. HUTCHMED (China) Limited recently secured a $400m upfront from Takeda for a vascular endothelial growth factor (VEGF) antibody, while Akeso Inc. negotiated $500 million up front as part of a $5 billion potential deal with Summit for its PD-1/VEGF bispecific antibody. Companies that have already licensed assets can consider converting milestones and long-term revenue potential with non-traditional investors such as royalty purchasers.

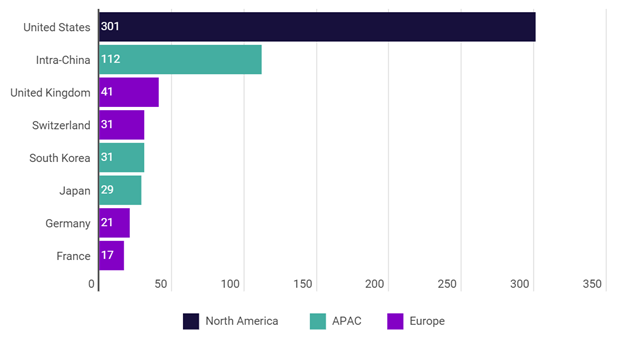

Considering the strength of the local pipeline, there will also be a tremendous amount of value to be made within China’s own borders. Indeed, around 16% of alliances signed by Chinese companies since 2019 have involved the exchange of technologies or developmental rights with a domestic partner (see Exhibit 3). Companies that are already at the commercial stage can source complementary assets to build a comprehensive portfolio and grow revenues within the China market itself. From this starting point, domestic consumption has the potential to act as a foundation for stable growth. In time, this will allow the development of commercial capabilities in international markets ― perhaps the ultimate endgame for the globalization of the Chinese pharma industry.

Exhibit 3: Top Partner Location for Chinese Alliances

Source: Citeline, Biomedtracker

Rome Wasn’t Built in a Day

All the ingredients are present for the next world-leading biotech company to emerge out of China. This is undoubtedly happening in other high-tech industries, although the slower-moving and highly regulated nature of pharmaceuticals means that patience is required. Coupled with the near-term funding challenges, we are unlikely to see a breakout within the next few years. That said, with the scale of innovation taking place in China, and the vast revenue potential on offer as health care expenditure grows, such a breakthrough would appear to be inevitable. While running hard for the finish line, it remains important for Chinese and other firms to embrace a steady growth trajectory and invest within a company’s means, and within its own borders. Solid business fundamentals will enable Chinese companies to develop and retain the next generation of therapeutic breakthroughs, but this can only be achieved through careful planning and deliberation, and by having a realistic perspective on global drug development and regulatory timelines; good ideas and hard work count for nothing if they are squandered through short-termism, a lack of adequate planning or overly hasty execution.

US companies have captured much of the value of checkpoint inhibitors, while Europe will be able to ride the GLP-1 wave. Perhaps it will be Chinese biotechs that will unlock the commercial potential of cellular or genetic therapies at scale over the next several years.

JUL 13, 2023

Press Release

Clinical

Citeline Appoints Clinrol as Strategic Clinical Trial Partner Across APAC Region

Citeline announces a strategic partnership with Clinrol, a clinical trial recruitment company, to expand and enhance patient recruitment for upcoming clinical trials across the Asia-Pacific (APAC) region.